Just prior to leaving for my client yesterday I received an e-mail from the English Setter Rescue. A lovely girl was in the King William pound and today was the "Day". Times up, out or down. She had a foster, but the foster was up in DC and could not take her until Tuesday.

I found myself writing one of those 'use me as a last resort' e-mails. I was extraordinarily busy, and would have to leave early. I don't have a completely fenced in yard, and English Setters are go-go guys and gals. So all I could think about was all of the obstacles to my getting her--particularly when I had to do a rescue the next day (today). Stepping back away from the obstacles, though, I had to reason with myself, that I literally was the singular intervention in this dog's life on that day--and that felt like a duty. Not a burden, but simply a duty. I hit the send button.

My cell phone rang immediately. As it turned out, another volunteer who could not get her, could overnight her. All I had to do was drive. King William is not very far out. It was about a 40 minute drive. I picked up this BIG girl, who was very reticent, but very sweet (as are most ES's). Driving back into town, I was headed west. I was treated to the most beautiful and luminous of sunsets. It felt like a reward for doing good.

We will have a cold day today to do our work. I like doing these rescues in the cooler (if not cold) months. I don't get overheated, and the dogs do not get overheated. You can service the pups and their crates and stick them right in a vehicle without baking them.

The market has gone no where so it seems. I did get a call from a Merrill Lynch person who had been talking to my client about their investment options for the 401(K). He was going on and on about their experience. And then started talking about how they like corporate bonds and muni's. (I'm sure 2 years ago they liked the CDS's). Generally, he was talking about their 'success'. I had a 'moment' and said, "Well, after all you've done so well on your own account." I don't think that he fully understood my meaning.

Permit my being a little jaded in taking investment vehicle advice from someone who had to have a shotgun wedding.

Saturday, January 31, 2009

Thursday, January 29, 2009

The Market?

I'm now on day 8 of my consulting project. So far nothing has blown up. I was able to process and get payroll out with nary a glitch. The nice thing about seeing and working with lots of systems, is that you realize that there are only so many different ways to get to the end result. The software interface either makes it an efficient or frustrating experience. And....I learned a long time ago that you do not mess with people's pay. So, I spent the better part of the weekend entering, checking and double checking payroll. It's an environment with producing employees so there is job costing involved for 80% of the employees.

But I've had to sit in an emptied seat and figure it all out for myself for every job that I've ever had (consulting and employee). While it's not a comfortable experience flying an airplane blind, I'm an intrepid pilot--though I would likely never land a plane so smoothly on the Hudson. The trouble is that these positions are pretty isolated and not one other person in the company knows how to do anything that seat does. They all just know what they get from the seat.

Being away from the market, I'm reminded as to what a foreign world the market's daily machinations are to working folk. The respite away from the dips, soars and wiggles has been very refreshing. I still look at charts, mind you, and I'll look at a few after I press the send button.

I had to have my car serviced. I stopped by to visit my salesman--he is a professional salesperson, and if you buy a car from him, he will take care of you. You will find NO auto salesperson more successful than he. My husband and I have bought every Ford car we've owned from him. He's been at the same dealership for years, except for a little tiff he had and left for a very brief interlude to work for a competitor. He said his volume is down 50% and his income is down 70% as they are offering employee discounts to customers to move product.

I heard Dennis Gartman on Gary K night before last. He believes, as does many others, that the market has already bottomed. I'm trying to be agnostic. I've enough long exposure to not feel like I'm missing out on any of the the good moves.

I've been watching the Utilities. I have some FEB XLU 30 calls. Lots of constructive action in several names.

Today I hunt for W-2's.

But I've had to sit in an emptied seat and figure it all out for myself for every job that I've ever had (consulting and employee). While it's not a comfortable experience flying an airplane blind, I'm an intrepid pilot--though I would likely never land a plane so smoothly on the Hudson. The trouble is that these positions are pretty isolated and not one other person in the company knows how to do anything that seat does. They all just know what they get from the seat.

Being away from the market, I'm reminded as to what a foreign world the market's daily machinations are to working folk. The respite away from the dips, soars and wiggles has been very refreshing. I still look at charts, mind you, and I'll look at a few after I press the send button.

I had to have my car serviced. I stopped by to visit my salesman--he is a professional salesperson, and if you buy a car from him, he will take care of you. You will find NO auto salesperson more successful than he. My husband and I have bought every Ford car we've owned from him. He's been at the same dealership for years, except for a little tiff he had and left for a very brief interlude to work for a competitor. He said his volume is down 50% and his income is down 70% as they are offering employee discounts to customers to move product.

I heard Dennis Gartman on Gary K night before last. He believes, as does many others, that the market has already bottomed. I'm trying to be agnostic. I've enough long exposure to not feel like I'm missing out on any of the the good moves.

I've been watching the Utilities. I have some FEB XLU 30 calls. Lots of constructive action in several names.

Today I hunt for W-2's.

Sunday, January 25, 2009

Cecil County SPCA

I adopted Daisey from this organization, and I have given them support. I stopped sending any further donations as no one bothered to send me a thank you note. Recently, I was both surprised and disgusted to learn of the many allegations by former shelter workers and volunteers of animal abuse. One of our transport volunteers for my Saturday transport voiced some concerns. Apparently, many have been trying to get their voices heard to get someone to do something. I'll spare you the details. I had to stop reading the affidavit that was forwarded to me after about line 3. The alleged cruelty is unspeakable. Though someone had to speak it to fill out the affidavit. Worse, this person (and others) had to witness it. Worse still, the animals had to experience it.

Hopefully the tenor of the accusations is to the level that something will be done to remove the management of that facilty and return the facility to what it is supposed to be: a shelter.

Hopefully the tenor of the accusations is to the level that something will be done to remove the management of that facilty and return the facility to what it is supposed to be: a shelter.

Friday, January 23, 2009

The Nature of Risk Part Two

Justin Mamis's book, The Nature of Risk, is now on my 'must recommend' list for new investors. I'm not longer a new investor, but I sure learned plenty from it. There is a mosaic of points that he makes about time, price and information risk that is so cogently said, that I've not considered them together in such a way. Consider these points. . .

* At the bottom, there is maximum negative, and no positive, information, but the price risk is minimal. (p 36). . . The price risk--because selling is exhausted--has been taken out of the stock, even though we have total information risk.... At the moment of maximum information risk, the price risk is mininal.

* The more information that becomes available, the greater the price risk because the stock has already risen (p. 42). . . Thus at the point of maximum positive information we also have maximum price risk.

* Time risk is alwasy present for those who are over anxious to bottom-fish.What does eventually turn out to be the bottom eighth--in hindsight--is a high-risk place to buy a stock. (p. 34)

Overheard

I overheard a money manager stating the importance of staying invested so that investors can catch the first meteoric rise off the bottom.....paraphrased......"being in such lifts off the bottom are important to not underperform the benchmark indices."

As individual investors, we are not compared in any mandatory way to any benchmark indices. Any such comparison is done voluntarily--or perhaps under durress by a spouse who wonders about our competency--sometimes with good reason. Assuming a measure of competency which has schooled us into stepping aside lest we get flattened by an avalanche of selling activity, we have a heckuva lot outperformance goodwill accrued as we've sidestepped a wholesale 40%+ haircut on our portfolio. Why, then, should we feel compelled to step into the opaque and turbulent waters of a market uncertain as to if its next move is up or down?

Why are there few money managers willing to say such? Who's to know. But even forgetting about any of that, and I do not believe in benchmark performance against indices. Relative outperformance against an absolute loss of dollars is a hollow victory. John Hussman is astute in pointing out that the best way to compare the performance of one's money manager is over the course of an ENTIRE cycle. Makes sense to me.

As individual investors, we are not compared in any mandatory way to any benchmark indices. Any such comparison is done voluntarily--or perhaps under durress by a spouse who wonders about our competency--sometimes with good reason. Assuming a measure of competency which has schooled us into stepping aside lest we get flattened by an avalanche of selling activity, we have a heckuva lot outperformance goodwill accrued as we've sidestepped a wholesale 40%+ haircut on our portfolio. Why, then, should we feel compelled to step into the opaque and turbulent waters of a market uncertain as to if its next move is up or down?

Why are there few money managers willing to say such? Who's to know. But even forgetting about any of that, and I do not believe in benchmark performance against indices. Relative outperformance against an absolute loss of dollars is a hollow victory. John Hussman is astute in pointing out that the best way to compare the performance of one's money manager is over the course of an ENTIRE cycle. Makes sense to me.

Thursday, January 22, 2009

Vulnerable S&P

[This picture scroll illustrates a story of Minamoto Yoshitsune, a military commander at the end of the 12th century, and his follower, Benkei, who were expelled from Kyoto and arrived at Hiraizumi, Oshu Province. This story was very popular by being adapted to dramas and novels] Click pic to be transported to the Rare books of the National Diet Museum.

[This picture scroll illustrates a story of Minamoto Yoshitsune, a military commander at the end of the 12th century, and his follower, Benkei, who were expelled from Kyoto and arrived at Hiraizumi, Oshu Province. This story was very popular by being adapted to dramas and novels] Click pic to be transported to the Rare books of the National Diet Museum.I've some client work that will keep me away from the markets for some weeks/months. I'm reminded that my skills are best deployed to help others.

The S&P is looking very vulnerable to my eye. It will either hold or break. It is likely not to dawdle long here.

Up or down? Toss a coin.

Tuesday, January 20, 2009

How Low Can They Go?

Sounds like it ought to be a new game show for financial stocks. Here's an ugly picture

Who is left to sell BAC? Or C?

Here's a chart of Industrial Metal Prices.

Have they stabilized a la Napier's suggestion for a bear market to end? I do not know. The $USD action and supply/demand are sort of a jumble. Best to observe as this violence plays out.

Have they stabilized a la Napier's suggestion for a bear market to end? I do not know. The $USD action and supply/demand are sort of a jumble. Best to observe as this violence plays out.

Who is left to sell BAC? Or C?

Here's a chart of Industrial Metal Prices.

Have they stabilized a la Napier's suggestion for a bear market to end? I do not know. The $USD action and supply/demand are sort of a jumble. Best to observe as this violence plays out.

Have they stabilized a la Napier's suggestion for a bear market to end? I do not know. The $USD action and supply/demand are sort of a jumble. Best to observe as this violence plays out.

Monday, January 19, 2009

I Couldn't Help Myself

I no longer color my hair. Though I must say that it is a bit unsettling when folks say about one's streaks of gray that it looks "striking". It makes me think of Morticia. I'm not contemplating a divorce quite yet. So the agent of change in my life must be this blog.

I found this template and I like it alot. I have to rebuild links and what not. I hope you like the new style.

I found this template and I like it alot. I have to rebuild links and what not. I hope you like the new style.

S&P 500: Then V. Now

In my continuing quest to bring you stuff that no reasonable person would look for on his/her own, I present to you the following table that shows the change in relative market cap among the sectors represented in the S&P 500. You can get this information for yourself here

While an immediate review of the percentages themselves may produce a yawn or two, if you look at the % change over 2008, the change is rather stark.. . .

- Consumer Staples increase of 22.6%

- Energy being weighted just higher than Financials

- Financials DECREASING a whopping 34.6%

- Healthcare increasing 19.3%

- Utilities, while still less than 5%, increased 14.1%

I don't pretend to have any special knowledge of stuff, but given the weighting changes, it would seem to me that sector rotation would have lots to do with the behavior of the index when one is looking at comparisons. For example, how much further could financials fall RELATIVE to Consumer Staples? Meaning the new composition may affect onward rate of change relative to economic conditions. Accordingly, there might be some stability now in the index itself as so much of the 'hot money' was in Financials and Energy.

The S&P market cap has fallen 39.3% over the study period.

P. S. If I ever had ANY doubts about Mercury Retrograde, they were all resolved on our last dog transport: car troubles, traffic troubles, dog mix up troubles----not to mention the geese and the plane................

Sunday, January 18, 2009

The Nature of Risk

Google books on line has several out of print books that you can get. You know one of my favorites is Selden's Psychology of the Market. I think I'll go through that again today by the fire.

Anyway, this one came from Gold Bricks of Speculation

byJohn Hill, Jr. of the Chicago Board of Trade. (1904). It is helpful to read these long forgotten words to remind ourselves that there is truly nothing new in the world, and people cheating other people is a timeless preoccupation of humankind.

byJohn Hill, Jr. of the Chicago Board of Trade. (1904). It is helpful to read these long forgotten words to remind ourselves that there is truly nothing new in the world, and people cheating other people is a timeless preoccupation of humankind.Fraser Publishing has a number of these books for a reasonable price. I recently finished Justin Mamis's The Nature of Risk: Stock Market Survival and the Meaning of Life. It is a delightful book about the market and the rather twisted ways in which our psychology perceives risk. In reading the forward, he mentions Helene Meisler who write TA for Real Money. I wrote her a brief e-mail mentioning how much I enjoyed the book. She said that Mamis was the best mentors that a person could have. He is in his eighties now. How delightful it must be to have your mentor call you out as being a "helper along the way" to his/her own understanding.

As I move along in seeking to diminish the perplexedness out of my own investing, I've found that the less I think, the better I do. I say this, though, having spent a good bit of time in forging my own understanding of stock market stuff--and developing a bit of 'doing without thinking' which is rather firmly rooted in doing a lot of thinking, doing, falling down, getting up and getting kicked in the stomach, arse, and having my ears boxed by the market. It's called building competence.

I have to compare my investor education to the exquisite trade of a blacksmith. With only fire and brawn and a rhythmic pounding of his hammer, he takes unformed metal and makes it into wondrous things of both elegance and utility. I'm pushing for both elegance and utility in my own investor education. The fire is my own desire to understand this 'stuff' and the brawn is simply my dogged tenacity in reading and acquiring the tools to be successful and applying those tools in an environment of uncertainty (risk).

Mamis is a market technician's technician. He believes that the market has its own language and uses technical analysis to listen to what the market is saying. He reminds that the market is designed to fool the most people most of the time. I believe him.

He writes

The value of technical analysis in the stock market is to reduce risk. It is especially helpful in guiding you to believe what otherwise seems unacceptable. By extension, therefore, it is most helpful at identifying significant market turns, both for the market and for individual stocks. . . . Stock charts and the indicators are like doctors' advice: exercise, diet, reduce stress, and so on. They are a means of establishing imperfect but relatively objective ways to understand market risks and market choices. (p.13)

This book reads more like an engaging philosophical treatise that doesn't mention words such as phenomenology! Also, his writing is fluid and engaging, and the book is liberally interspersed with real nuggets of practicable wisdom. I'll likely read it a couple of more times. What is particularly helpful is his discussion about ultimately you have to make a decision to act (buy/sell/hold) within a context of having incomplete (in all of its manifestations) information.

Tuesday, January 13, 2009

Mercury Retrograde Strikes at Home

In classic Mercury retrograde fashion my computer was mightily felled over the last couple of days. I wrote to Cox customer service and they gave me the standard suggestions which I had done. But my broadband was crawling at 512kbs. All things that I rely on my computer for were screwed up. In that process, I wanted to share a few things with you.

- Norton Utilities: I found and ran Stopzilla--one of those anti-spyware programs. It found Vundo and another virus that Norton was asleep at the wheel with! It has since found some other stuff.

- Speedtest.net: Here's a great place to test your internet upload/download speed. My neighbor who has been in computer sales, repair etc recommended this site. This is where I was able to measure my pitiful performance. Check it out.

- Online PC Repair: AFter I pulled off a bunch of stuff, these guys did a PC tuneup/repair that found bunches of other crap that both Stopzilla and Norton did not remove. For a flat fee, they fix this stuff. I got the Family Premium Membership which gives unlimited service for 1 year on up to 3 computers. The cost was $380. My daughter has a laptop, and just doing two tuneups/fixes pays for the service--then you can get whatever you need for another year afterwards. Sure beats unhooking and hauling. These guys worked on the computer (I couldn't use it for a good part of the day). Their service was terrific and more than exceeded my expectations. (I don't get any freebies for mentioning them).

Sunday, January 11, 2009

Mercury Retrogrades for 2009

Yes dear readers we are going to dip our toe into the waters of the fantastical other realms, in this case astrology! Whether or not you believe it or not, why not throw some salt over your shoulder and mark the dates below on your calendar for this year? These are the dates that Mercury goes into retrograde. These periods mark a time when stuff ruled by Mercury can go awry.

'SRx' is' retrograde'. 'SD' is 'station direct' where the planet moves from retrograde to forward motion. Here's a nice summary of the effects of a Mercury retrograde:

Mercury retrograde gives rise to personal misunderstandings; flawed, disrupted, or delayed communications, negotiations and trade; glitches and breakdowns with phones, computers, cars, buses, and trains. And all of these problems usually arise because some crucial piece of information, or component, has gone astray or awry.

Rob Tillet (Click here for link to this article)

Tillet also notes:

In general, Mercury rules thinking and perception, processing and disseminating information and all means of communication, commerce, education and transportation. By extension, Mercury rules people who work in these areas, especially people who work with their minds or their wits: writers and orators, commentators and critics, gossips and spin doctors, teachers, travelers, tricksters and thieves.Because of the 'tricksters' and 'thieves' inclusion above, this retrograde fully embraces the market! Supposedly this is also a time when technical analysis, specifically supports, signals etc fail.

Saturday, January 10, 2009

Books and Candles

Because I am a reader, I'm an easy person to buy gifts for. Gift

certificates to Barnes and Noble or Amazon are generally in my

possession this time of year. Last evening I spent some time choosing

some

- "Meditations on Quixote"; Jose Ortega y Gasset; Paperback

- "Trading Without Gambling: Develop a Game Plan for Ultimate Trading Success (Wiley Trading)" Marcel Link; Hardcover

- "The Ascent of Money: A Financial History of the World"; Niall Ferguson; Hardcover; $17.61

- "When to Sell: Inside Strategies for Stock-Market Profits (Fraser Publishing Library)";Justin Mamis; Paperback

- "The Nature of Risk (Fraser Publishing Library) (Contrary Opinion Library)" Justin Mamis; Paperback;

investment, but rather a trade. My current philosophy is to create

'dividends' through small exposures of capital to what appears to my

eye to be good chart set ups.

I hear on CNBC many money managers coming out with the 'paid-to-wait' theme by encouraging the investment in companies that pay a dividend. I remember when GM had a

.50 quarterly dividend. Had you hung on to that, you'd been paid to

watch your investment evaporate. Same can be said for the bank stocks.

Utilities, another dividen payer, have not faired too well either. The

siren like call for dividends can lead you on the rocks if you are not

careful. It is not a story that I buy, but it makes sense for some. But

the paid to wait is a stupid argument if the stock is under pressure. A

4% yield against a 10% + drop in price is not a trade off that I find

attractive.

I spent a goodly amount of time over the holidays

scouting out stocks. Last week, I had 18 positions (which is quite a

bit for me). Of those 18, 14 were green, 2 which were hedges were red

and 2 were red on their own. The reds were modest. Two stocks below,

I'm particularly proud of: BEST and CNTF--two of my Chinese take out

(meal, not buy out) stocks. I shared those with you when I bought them.

I

Ishould add that BEST is VERY thinly traded. The nice thing about being

a nobody is that unlike BIG money, I can buy stuff like that. I've

shown in green where I bought these stocks. Id bought them because (a)

I liked the chart pattern (basing action, spike in volume); (b) I liked

the fundamentals. That two-fer made it less risky.

To say that the move has been remarkable is an understatement. I

judiciously sold into this rise for CNTF, and currently just have

"house money". Yeah that is another aphorism where you can still piss

money away if you don't have to! When you buy a stock for .89 per

share, and it makes a move such as the above, to NOT lock in partial

profits is just plain foolish. However, I have a long history of

selling way too early.

There is an aphorism that "No one ever went broke by taking profits."

Like most things in life, context matters. And in the context of

buying/selling stocks, if you have 5 losers that you lost 7-10% on, and

1 monster winner that you settled for a 20% profit (when it later went

on to be a 4 bagger), then you just squandered an opportunity to undo

alot of ill on stock picks of lesser genius. (Yes, I understand that it

is not genius but rather managing probabilities!).

One of my goals this year is to find a better way to manage

profits--finding that balance between selling too soon and holding on

too long. The space between those two polarities is where I want to

be. I rarely hold on too long. But I've lost mucho dinero

(opportunity costs) in bailing too soon. And opportunity cost is a

cost--it just doesn't show up on your portfolio statement, but your

mind calculates it in its "you're a dumb ass" bucket. It's the same

place that all of your memories that make you privately blush because

you couldn't believe that you were so stupid to do or say a certain

something that you went ahead and did or said despite knowing better.

It's definitely a place where you don't want your bucket to runneth

over, so limiting what you add to it is of some merit. Naturally

bailing on a stock too soon and not bailing soon enough are all

additive to this bucket.

Now having said all that, you immediately realize why the market and

your participation in it is like being in an insane asylum. Fear of

selling too late or selling too soon could render one paralyzed by self

doubt. You can immediately see, then, my choice of books above.

Knowing when to buy (which I do think that I've mastered pretty well)

and knowing when to sell (I wouldn't be talking about the DA bucket if

I were any good on this!) is the second part of the equation. And of

course, both of those things reside in the context developing a game

plan.

The Ascent of Money is a book club selection. We are resurrecting our

book club, and that will be our next selection. I'll be hosting book

club. I've plenty of time to think of what to fix. Jose Ortega y

Gasset is an old favorite of mine. You'll remember that I found a

couple of his books at the used bookstore in Sylva on our trip to

secure Ella. Meditations on Quixote was his first book. And as I write this, I'm going to put a reading of Don Quioxote on my list of

things to read this year.

And speaking of resurrection....I've pulled out my Candlestick Charting Explained. by Gregory L. Morris. This is after having re-read completely through Martin Pring's Technical Analysis Explained as well as John Murphy's TA book earlier. While I generally use candlestick charts--I cannot say that I've any real focused study on them. So as part of my managing my positions better, I'll be sharpening my chart reading skills on candlesticiks.

Friday, January 09, 2009

Buy and Hold

I'll go to my grave convinced that the buy and hold is a scheme by the financial services industry to dupe (lull) hapless investors into a sense of false security. Ultimately, passive money managers have no real interest in YOU, but a very keen interest in YOUR MONEY. I know that I'm painting with a wide brush here, which is unfair and all of that.

However, when I meet with my friends, and they lament about the market and their lost wealth, it makes me sad. I come from a working class family. My mother and father had to work for everything that they had. My husband and I have had to work for everything that we have. There's no systematic wealth transfer on my or my husband's side of the family. No grandparents able to fund college educations. Many of my friends, even though they are professionals, come from the same working stock.

These losses, then, hurt. I had dinner last evening with a couple of friends. And they were kind enough to ask me about what I thought the market would do. They trust my opinion because I've been right. Unfortunately, as I was the only person in their sphere (I certainly wasn't the only one expressing concerns) , talking about this stuff, I'm sure that they thought I was a bit of a crack pot.

I'm also careful to clarify that just because my opinion was correct on one large matter, I could get other matters totally wrong. But they asked me, "Do you think that the market is done going down, and do you think that it will come back?" I assured them that nobody knew the answer to that question. My opinion, no better than any other's, was that the market was showing improvement, but I believed that it would go down again and that it would be long recovery. I talked about the similarities with Japan. Japan is a useful example of hope gone terribly awry--for more than 20 years.

While many want to pooh-pooh Japan, it is the second largest economy of the world. And when folks point to the Great Depression and the massive bull market that sprang from that ash heap, it was a time when we actually produced something that others wanted. Surely some other wellspring of economic prosperity may spring from the scorched earth. Outside of the government's stimulus plan, I'm not sure that I see it clearly. There's a shadowy glimmer of energy efficiency--and with Russia and Iran sabre rattling and chest beating, quite a bit of money and energy may get behind improving our reliance on petroleum.

It is Armageddon week on The History Channel. So long as your funds can hold out until 2012 when the world is likely to come to an end through the bible coders, the end of the Mayan calendar, the Cardinal Climax and all other confluence of signs: natural, supernatural, supranatural and paranoid.

While my friends felt depressed about the economy and the market, I did state that I thought that the US would weather it better than most places. But I ended that portion of the conversation with the counsel: You do NOT have to expose your assets to the stock market when it is at its riskiest. The retort, "How do you know when to sell?"

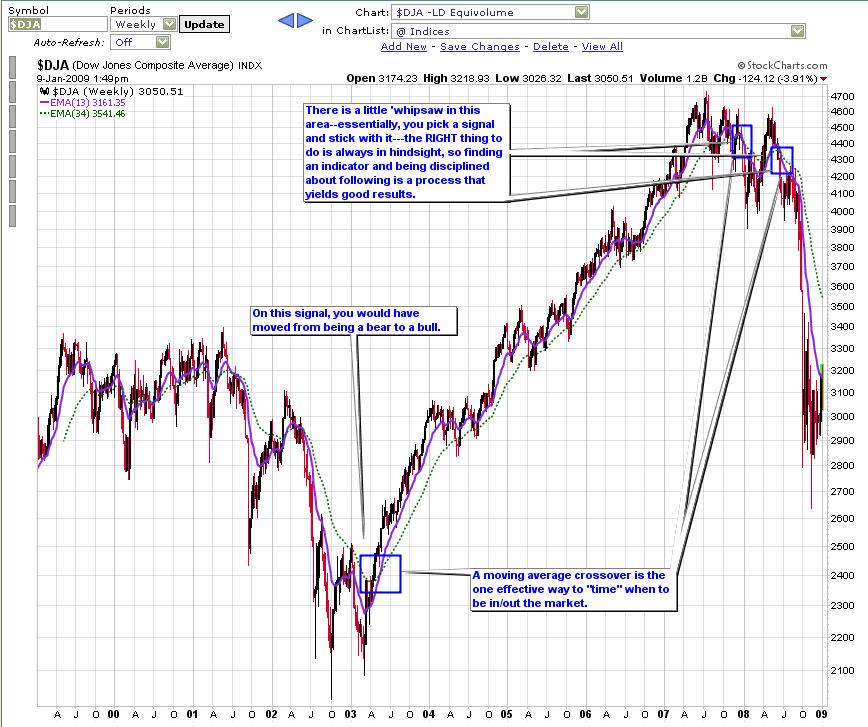

First, I admit that I spend a great deal of time studying the market and improving my investor skills. Second, most folks have neither the time nor the inclination to do that sort of thing. Accordingly, how does one meld the first and second point together? My advice to someone who wants to protect their capital but have appropriate exposure to new uptrends would simply be this: On a month basis, look a total market indicator that has a short term and long term moving average. Buy when the s-t average crosses from below to over the l-t average. Sell when the s-t average crosses from above to over the l-t average. One could use the 50/200 combination. I've been using the 13/34 in my charts.

Without inviting a debate on which is better (my analysis was merely to get the s-t v. l-t relationships together to share with my friend), I created this chart.

Admittedly the period prior to 2002 had much chopping around!But I am making a quick example here rather than providing a be-all methodology to smooth out the rough patches. My point specifically was to demonstrated for my friend was that while you cannot time the market perfectly, you can certainly make entries and exits that expose your portfolio to the gains and protect your capital from the great swooshes down.

Why have your money with a passive money manager who collects a fee and only puts you in in passive investments? Where's the value if in a down market you are going to lose right along with indexes? Personally, I don't see any value to that and in fact, it seems to me to be pretty darned expensive.

However, when I meet with my friends, and they lament about the market and their lost wealth, it makes me sad. I come from a working class family. My mother and father had to work for everything that they had. My husband and I have had to work for everything that we have. There's no systematic wealth transfer on my or my husband's side of the family. No grandparents able to fund college educations. Many of my friends, even though they are professionals, come from the same working stock.

These losses, then, hurt. I had dinner last evening with a couple of friends. And they were kind enough to ask me about what I thought the market would do. They trust my opinion because I've been right. Unfortunately, as I was the only person in their sphere (I certainly wasn't the only one expressing concerns) , talking about this stuff, I'm sure that they thought I was a bit of a crack pot.

I'm also careful to clarify that just because my opinion was correct on one large matter, I could get other matters totally wrong. But they asked me, "Do you think that the market is done going down, and do you think that it will come back?" I assured them that nobody knew the answer to that question. My opinion, no better than any other's, was that the market was showing improvement, but I believed that it would go down again and that it would be long recovery. I talked about the similarities with Japan. Japan is a useful example of hope gone terribly awry--for more than 20 years.

While many want to pooh-pooh Japan, it is the second largest economy of the world. And when folks point to the Great Depression and the massive bull market that sprang from that ash heap, it was a time when we actually produced something that others wanted. Surely some other wellspring of economic prosperity may spring from the scorched earth. Outside of the government's stimulus plan, I'm not sure that I see it clearly. There's a shadowy glimmer of energy efficiency--and with Russia and Iran sabre rattling and chest beating, quite a bit of money and energy may get behind improving our reliance on petroleum.

It is Armageddon week on The History Channel. So long as your funds can hold out until 2012 when the world is likely to come to an end through the bible coders, the end of the Mayan calendar, the Cardinal Climax and all other confluence of signs: natural, supernatural, supranatural and paranoid.

While my friends felt depressed about the economy and the market, I did state that I thought that the US would weather it better than most places. But I ended that portion of the conversation with the counsel: You do NOT have to expose your assets to the stock market when it is at its riskiest. The retort, "How do you know when to sell?"

First, I admit that I spend a great deal of time studying the market and improving my investor skills. Second, most folks have neither the time nor the inclination to do that sort of thing. Accordingly, how does one meld the first and second point together? My advice to someone who wants to protect their capital but have appropriate exposure to new uptrends would simply be this: On a month basis, look a total market indicator that has a short term and long term moving average. Buy when the s-t average crosses from below to over the l-t average. Sell when the s-t average crosses from above to over the l-t average. One could use the 50/200 combination. I've been using the 13/34 in my charts.

Without inviting a debate on which is better (my analysis was merely to get the s-t v. l-t relationships together to share with my friend), I created this chart.

Admittedly the period prior to 2002 had much chopping around!But I am making a quick example here rather than providing a be-all methodology to smooth out the rough patches. My point specifically was to demonstrated for my friend was that while you cannot time the market perfectly, you can certainly make entries and exits that expose your portfolio to the gains and protect your capital from the great swooshes down.

Why have your money with a passive money manager who collects a fee and only puts you in in passive investments? Where's the value if in a down market you are going to lose right along with indexes? Personally, I don't see any value to that and in fact, it seems to me to be pretty darned expensive.

Wednesday, January 07, 2009

Learning from the Great Ones

Wang Jin

Wang JinI had a couple of books arrive yesterday. One of them is a regrettable choice: Learning Learning from Data: Concepts, Theory, and Methods from Data: Concepts, Theory, and Methods, Cherkassky, Mulier. The idea of the book is for people who must understand the principles and methods for learning dependencies from data. If I get through this book, I might as well read Krugman's series. It is a dense volume.

The other book was a slim and easily read volume, Lessons from the Great Traders, John Boik. He has a website and a tab for "Monster Stocks, the name of his most recent book. There's some names posted that you might find interesting.

It is always refreshing to read about successful investors. It was affirming to read that each of the investors that Boik profiles (Darvas, Livermore, Baruch, O'Neil) each went through a learning process that involved skinned up knees and kick or two in the stomach and ass. Nevertheless, they learned from their mistakes and ultimately prevailed.

As Boik notes, there is nothing easy about making money in the stock market. There is certainly the perception that choosing winning stocks is easy--and that is ultimately the allure. I think that Stan Weinstein said it best: That the market's objective is to take the money out of the pockets of many and put it in the pockets of a few. There's also a perception that when you buy a stock in a raging bull market, your performance is directly linked to your genius. It's not easy and everyone looks like a genius in a bull market.

You may also find some well done articles at Market Masters. Lots of good stuff at that website. I go back and re-read the profiles, again for knowledge and inspiration. I particularly like the article on Richard Donchian (maybe because of his Armenian heritage!). But there are some timeless investment/trading rules here that you may wish to print out and post handy to your workspace.

As I think about my own bumpy process as an investor, I realize that my embrace of these books was through shared experience: I made all the mistakes that they made. Accordingly, reading about these very successful investors doing the same assuaged a bit of the shame and embarrassment of having committed those same errors.

Overconfidence, not knowing what you do not know, lack of discipline all conspire against one's investment success.

Sunday, January 04, 2009

Napier's, Anatomy of the Bear: Lessons from Wall Street's Four Great Bottoms

I was researching Tobin's q-factor, which led me to Russell Napier's excellent book. I wanted to capture a few salient points (there are many) in Russell Napier's, Anatomy of The Bear. You can also listen to Jim Puplava's interview with Napier here. ( Jim has many terrific guests on. Great interviews you can listen to while you are cleaning your desk off and paying bills.) Napier says it best:

Napier chose four bear markets (month equates to the bottom):

His book is essentially a field guide to the 'signs' of a bear market's bottoming process. Accordingly, if you have an interest in reading about the confluence of 'stuff' surrounding bear markets, I'd recommend your reading this book and plowing through it. While I enjoyed the book, but there are places where the writing could have been clearer and the data presented a bit more clearly. Nevertheless, there is much factual data that will give an investor some armament against the foolishness spouted by pundits.

Napier notes some key items to look for--I highlighted the first two because they were evident at each of the bear markets he studies--he particularly notes copper prices as the commodity to watch:

By watching the financial bears, we can observe the point at which a number of potential factors come together to signal the market can only get better. Those factors include low valuations, improved earnings, improving liquidity, falling bond yields, and changes in how the market is perceived by those who play it. (p. 3)

Napier chose four bear markets (month equates to the bottom):

- August 1921

- July 1932

- June 1949

- August 1982

His book is essentially a field guide to the 'signs' of a bear market's bottoming process. Accordingly, if you have an interest in reading about the confluence of 'stuff' surrounding bear markets, I'd recommend your reading this book and plowing through it. While I enjoyed the book, but there are places where the writing could have been clearer and the data presented a bit more clearly. Nevertheless, there is much factual data that will give an investor some armament against the foolishness spouted by pundits.

Napier notes some key items to look for--I highlighted the first two because they were evident at each of the bear markets he studies--he particularly notes copper prices as the commodity to watch:

- improving demand at lower prices for selected goods, particularly autos

- commodity price stabilization

- improving economci news being ignored by the market

- rising volumes on a strong stock market

- falling volumes on a weak stock market

- a rising short interest

- a final fall in equity prices on low volumes

- reductions in Fed controlled interest rates

- A rally in the government bond market

- a rally in the corporate bond market

- positive signals from the Dow Theory

- Extreme undervaluation in the market: I partly produced by a final downdraft in prices. The second contributor is the failure of stock prices to keep up with economic and earnings growth. (p 37) [I do not see that we have the second contributor yet. It's also worth noting that there can be large gaps (2 decades in 1899-1921) of GDP growth without a commensurate increase in the earnings of companies--Napier notes a 130% increase in earnings v a 738% increase in GDP in 1881-1921 period. ]

- Napier calls into question the aphorism "buy when the news is bad". "The Wall Street Journal in the summer of 1921 was teeming with news and well-informed opinion that the economic contraction and with it the bear market in stocks was ending." (p.44). Specifically he opines that ". . . waiting for an absence of good news before buying stocks would not have been wise."

- Price stability is at the core of factors signaling the end of a bear market. Napier specifically notes that "the most accurate forecasts of the end of the bear market came from those who focused on the change in the trend in prices." He also notes specifically auto sales (demand response to lower prices) and copper prices. [I'll add that my focusing on the decline in the industrial metal prices helped me conclude that the good times were over. Industrial metal prices are starting to now recover. I watch Stock charts $GYX, which currently shows some recover. How long it will last will unfold in the fullness of time).

- A final bottom is generally made on low volume (in contrast to the popular adage). (p 68). [This observation lines up well with Selden's comment that the market generally rises from a period of dullness--market tops are violent; market bottoms are dull. Could we then be seeing JUST a year long workout of a top with more to follow? 'More to follow' would certainly fit with some of the direr predictions (e.g. L. Yamada's 400-600 S&P).

- In 1932, the Fed started a wholesale purchase of treasuries (as they are doing now) and that scared foreign investors thinking that the dollar would be devalued against other currencies, thus they wanted to liquidate their dollar reserves. [I believe that the moves of other currencies against the USD is one of the most important things for us to watch. We are not a producer nation any more--we are a service based economy. The countries that produce stuff (everyone BUT the US) will want their currencies cheap relative to ours. So perhaps we will not see a dumping of Treasuries as many fortell.]

- Napier notes that the move from overvaluation to undervaluation can take well over a decade--and that the 1932 bear market was the exception, not the rule. (p. 116)

- Napier notes " There is often ample good and improving economic news at the bottom of the market. This all suggest the risk to investors at these extreme times may not be as great as often assumed. An investor need not buy equities based on his forecast that the economy will start to improve in six-to-bnine months. At the great bear market bottoms there is likely to be growing evidence the economy is already on the mend." (p. 264)

p.74

Russell smartly reminds us that all bear markets are different. I'm also going to state that what we are undergoing is a trans-generational move which effectively emasculates any's posturing of "In my 30 years in the market". I'm hearing much of that, and I'm going to say emphatically that in a trans-generations move, 30 years is an inside of that and therefore irrelevant. That's not to say that the market may just go the way that those pundits suggest--UP. BUT, my point is that 30 years v. a trans-generational move (should we be having one)doesn't quite cut the mustard.

What I found most helpful was Napier's discussion of the interplay of government bond prices, corporate bond prices and the equity markets. While he did not provide a table, I will do so for you.

Now, let's take a look as to when government bond prices bottom.

Based on MY reading of the data table (Is that not a monstrous head and shoulders that can NEVER go below the neckline!), it appears to me that interest rates bottomed here: 2007-08-09 5.41. Accordingly, I'm going to call that date, the bottom in government bond prices (I've no idea if I'm using the right data). However, there is some credibility to that date as it was just a week before the FIRST systemic risk crisis in the money markets. I'm going to use the Dow Jones Composite Average rather than the DJIA. It's worth noting that the market TOPPED about 1 month ahead of the government bond market bottoming. Please click on these images to prevent blindness.

To be true to Napier's use of the Dow Industrials, I provide that chart here:

To be true to Napier's use of the Dow Industrials, I provide that chart here: (I am lazily not bothering with corporate bonds.)

(I am lazily not bothering with corporate bonds.)Am I concluding that this is indeed the bottom? Truly, I do not know, but the exercise seemed a fair to conduct. Looking at the weekly volume patterns in both charts certainly lends some credence that we had a high volume sell off in Sept culminating in November of 2008. I'd also hazard a guess that given the great hedge fund unwind, we are UNLIKELY to see a re-visitation of these volume levels. However, we should expect to see some improvement over the weekly volumes. It does NOT appear to me that we've had a low volume sell off.

I've flagged a number of interesting things in Napier's book which I'll share here in no particularly order. IN addition to chronicling what was happening in the monetary and interest markets, Napier chronicled WSJ commentary in the 2-3 months on either shoulder of the bear market bottom. My point in sharing a few of these things with you is that what his researched uncovered is at odds with some of the conventional wisdom. I'm including my summary of his points and the page number on which the thought is expressed. Any direct quotations of text will be within quotation marks. My own thoughts/questions will be in brackets.

Thursday, January 01, 2009

DJ Sector Performance

The above table is the DJ Sector overview for the last 5 years. I've included the last month and the last week to show the relationship of the last week performance to the last month. Not sure if it means all of that much, but I wanted to view it.

Happy New Year

May we live the New Year with a heart filled with gratitude and love. Not an easy thing to do but certainly worthwhile pursuing.

I see my last post was December 23. I really did not have much to say! Whatever the market lacked in zip for most of the holiday week it made up for yesterday.

We had a handful of people over for dinner last evening. A smaller scale than I've done in the past both in guests and fare. Past NY's dinners have been a bit overtaxing on both my energy and my pocketbook. I didn't want to spend $400-500 entertaining (as I had already done another grand scale dinner earlier in the year); however, I still wanted to do something nice. Rather than an expensive piece of beef, I fixed duck leg quarters. I served them with caramelized onions and spinach and butternut squash ravioli with shallots/bacon/cream. Our dessert was a simple, but delicious lemon tart. I had nice wine. We had crab stuffed eggs and smoked salmon.

The dinner came together well, and there was no compromise on the 'wow' factor. The smaller scale allowed me to enjoy my guests. I've been guilty of very elaborate meals in the past, that frankly left me exhausted. Graham Kerr remarked in one of his books that one should never have more than eight for dinner. I've had 10 and 12 in the past, and it really is too much. You wouldn't think that two people make all that much of a difference, but when you think about pan and serving sizes (desserts, entrees, wine), not to mention the seating, it really does. One hates to chop the guest list, but I did this year.

I'll spend a little time over the next few days reflecting on this past year. Because I've had my resolutions close at hand (by my computer), I was pretty successful in keeping most of them. A few were just on the radar and did not get within firing range. Oh well. I'm most happy with my fitness goals being reached, though I've fallen off the wagon in these last few weeks. I'll do my resolutions on a "mind map" format again. I really found that helpful.

I've also kept Miyamot Musahi's Nine rules close by. Here are my favorites: I also have Musashi's 9 things even closer...my favorites. . . .

With respect to the market: I did better than most hedge fund and money managers. My retirement accounts are higher yesterday than they were at the beginning of the year. I could have managed a few positions MUCH better and been significantly higher--the biggest fish that got away were my DIA SEP 125 puts AND my DUG $35 calls. I've a tear in my eye thinking of all the money that I left on the table--5 figures in both. Oh well.

I started out the year with the Lucky 13 that was given as a stragegy

You would have lost 29% of your investment. I guess that was better than the 34% that the S&P was down, but still..... I know that we will continue to hear about the worst being over; the stock market recovers before the economy; etc..... As I've come to learn, sometimes the hard way, the market is an odd mix fact and fantasy, with the fantasy being largely attributed to the emotions and lore (such as the Lucky 13, Dogs of the Dow, Best Buying Days, etc) surrounding the market.

You would have lost 29% of your investment. I guess that was better than the 34% that the S&P was down, but still..... I know that we will continue to hear about the worst being over; the stock market recovers before the economy; etc..... As I've come to learn, sometimes the hard way, the market is an odd mix fact and fantasy, with the fantasy being largely attributed to the emotions and lore (such as the Lucky 13, Dogs of the Dow, Best Buying Days, etc) surrounding the market.

The simple fact is this: If you lose 30% of your capital, you will have to make 43% on your entire investment to become whole again before any accretion. There's alot of compounding that nobody talks about much in avoiding losses. If the amount of time spent yapping about "long term horizon" were spent on preserving capital, individual investors would be much better off--they wouldn't need a long term horizon to make up for substantial losses suffered. Unfortunately, investors are admonished that market timing doesn't work.

Let's just call it something else: asset allocation. That's what the other money managers call it, right? "WE are not market timers; we are asset allocators." Asset allocation is all about managing risk and reward. Managing risk and reward is also relevant to particular positions. Where I've MISSED substantial gains is by not properly evaluating the risk/reward on some very favorable positions. In the same breath, but certainly not meant to minimize the mistake, I've also avoided most of the risks that exposed others to outsize losses. My goal this year is to do a better job of managing risk reward.

I see my last post was December 23. I really did not have much to say! Whatever the market lacked in zip for most of the holiday week it made up for yesterday.

We had a handful of people over for dinner last evening. A smaller scale than I've done in the past both in guests and fare. Past NY's dinners have been a bit overtaxing on both my energy and my pocketbook. I didn't want to spend $400-500 entertaining (as I had already done another grand scale dinner earlier in the year); however, I still wanted to do something nice. Rather than an expensive piece of beef, I fixed duck leg quarters. I served them with caramelized onions and spinach and butternut squash ravioli with shallots/bacon/cream. Our dessert was a simple, but delicious lemon tart. I had nice wine. We had crab stuffed eggs and smoked salmon.

The dinner came together well, and there was no compromise on the 'wow' factor. The smaller scale allowed me to enjoy my guests. I've been guilty of very elaborate meals in the past, that frankly left me exhausted. Graham Kerr remarked in one of his books that one should never have more than eight for dinner. I've had 10 and 12 in the past, and it really is too much. You wouldn't think that two people make all that much of a difference, but when you think about pan and serving sizes (desserts, entrees, wine), not to mention the seating, it really does. One hates to chop the guest list, but I did this year.

I'll spend a little time over the next few days reflecting on this past year. Because I've had my resolutions close at hand (by my computer), I was pretty successful in keeping most of them. A few were just on the radar and did not get within firing range. Oh well. I'm most happy with my fitness goals being reached, though I've fallen off the wagon in these last few weeks. I'll do my resolutions on a "mind map" format again. I really found that helpful.

I've also kept Miyamot Musahi's Nine rules close by. Here are my favorites: I also have Musashi's 9 things even closer...my favorites. . . .

- Learn to see everything accurately;

- Become aware of what is not obvious;

- Be careful even in small matters;

- Do not do anything useless.

With respect to the market: I did better than most hedge fund and money managers. My retirement accounts are higher yesterday than they were at the beginning of the year. I could have managed a few positions MUCH better and been significantly higher--the biggest fish that got away were my DIA SEP 125 puts AND my DUG $35 calls. I've a tear in my eye thinking of all the money that I left on the table--5 figures in both. Oh well.

I started out the year with the Lucky 13 that was given as a stragegy

You would have lost 29% of your investment. I guess that was better than the 34% that the S&P was down, but still..... I know that we will continue to hear about the worst being over; the stock market recovers before the economy; etc..... As I've come to learn, sometimes the hard way, the market is an odd mix fact and fantasy, with the fantasy being largely attributed to the emotions and lore (such as the Lucky 13, Dogs of the Dow, Best Buying Days, etc) surrounding the market.

You would have lost 29% of your investment. I guess that was better than the 34% that the S&P was down, but still..... I know that we will continue to hear about the worst being over; the stock market recovers before the economy; etc..... As I've come to learn, sometimes the hard way, the market is an odd mix fact and fantasy, with the fantasy being largely attributed to the emotions and lore (such as the Lucky 13, Dogs of the Dow, Best Buying Days, etc) surrounding the market.The simple fact is this: If you lose 30% of your capital, you will have to make 43% on your entire investment to become whole again before any accretion. There's alot of compounding that nobody talks about much in avoiding losses. If the amount of time spent yapping about "long term horizon" were spent on preserving capital, individual investors would be much better off--they wouldn't need a long term horizon to make up for substantial losses suffered. Unfortunately, investors are admonished that market timing doesn't work.

Let's just call it something else: asset allocation. That's what the other money managers call it, right? "WE are not market timers; we are asset allocators." Asset allocation is all about managing risk and reward. Managing risk and reward is also relevant to particular positions. Where I've MISSED substantial gains is by not properly evaluating the risk/reward on some very favorable positions. In the same breath, but certainly not meant to minimize the mistake, I've also avoided most of the risks that exposed others to outsize losses. My goal this year is to do a better job of managing risk reward.

Subscribe to:

Posts (Atom)