However, when I meet with my friends, and they lament about the market and their lost wealth, it makes me sad. I come from a working class family. My mother and father had to work for everything that they had. My husband and I have had to work for everything that we have. There's no systematic wealth transfer on my or my husband's side of the family. No grandparents able to fund college educations. Many of my friends, even though they are professionals, come from the same working stock.

These losses, then, hurt. I had dinner last evening with a couple of friends. And they were kind enough to ask me about what I thought the market would do. They trust my opinion because I've been right. Unfortunately, as I was the only person in their sphere (I certainly wasn't the only one expressing concerns) , talking about this stuff, I'm sure that they thought I was a bit of a crack pot.

I'm also careful to clarify that just because my opinion was correct on one large matter, I could get other matters totally wrong. But they asked me, "Do you think that the market is done going down, and do you think that it will come back?" I assured them that nobody knew the answer to that question. My opinion, no better than any other's, was that the market was showing improvement, but I believed that it would go down again and that it would be long recovery. I talked about the similarities with Japan. Japan is a useful example of hope gone terribly awry--for more than 20 years.

While many want to pooh-pooh Japan, it is the second largest economy of the world. And when folks point to the Great Depression and the massive bull market that sprang from that ash heap, it was a time when we actually produced something that others wanted. Surely some other wellspring of economic prosperity may spring from the scorched earth. Outside of the government's stimulus plan, I'm not sure that I see it clearly. There's a shadowy glimmer of energy efficiency--and with Russia and Iran sabre rattling and chest beating, quite a bit of money and energy may get behind improving our reliance on petroleum.

It is Armageddon week on The History Channel. So long as your funds can hold out until 2012 when the world is likely to come to an end through the bible coders, the end of the Mayan calendar, the Cardinal Climax and all other confluence of signs: natural, supernatural, supranatural and paranoid.

While my friends felt depressed about the economy and the market, I did state that I thought that the US would weather it better than most places. But I ended that portion of the conversation with the counsel: You do NOT have to expose your assets to the stock market when it is at its riskiest. The retort, "How do you know when to sell?"

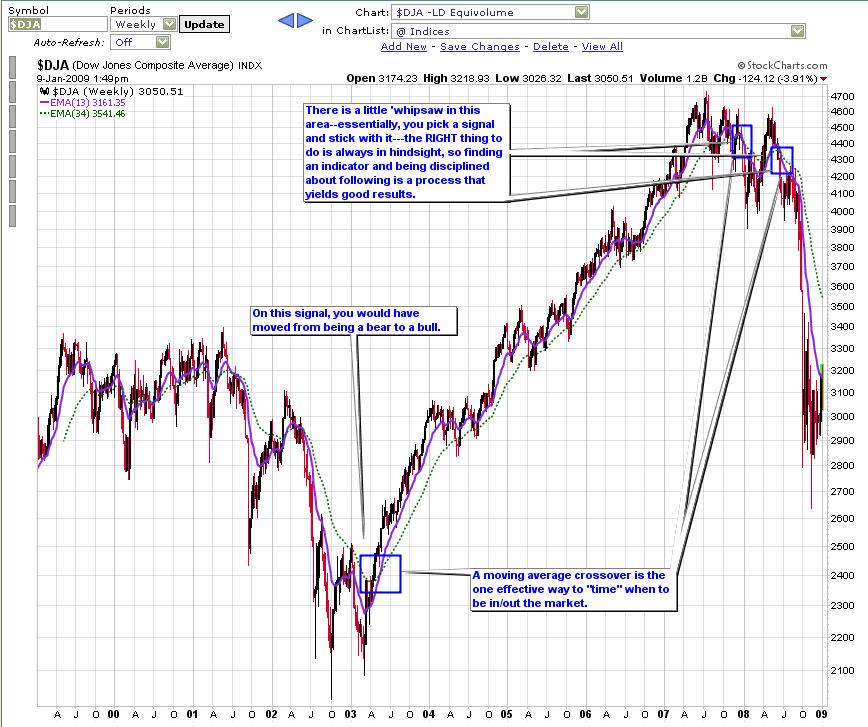

First, I admit that I spend a great deal of time studying the market and improving my investor skills. Second, most folks have neither the time nor the inclination to do that sort of thing. Accordingly, how does one meld the first and second point together? My advice to someone who wants to protect their capital but have appropriate exposure to new uptrends would simply be this: On a month basis, look a total market indicator that has a short term and long term moving average. Buy when the s-t average crosses from below to over the l-t average. Sell when the s-t average crosses from above to over the l-t average. One could use the 50/200 combination. I've been using the 13/34 in my charts.

Without inviting a debate on which is better (my analysis was merely to get the s-t v. l-t relationships together to share with my friend), I created this chart.

Admittedly the period prior to 2002 had much chopping around!But I am making a quick example here rather than providing a be-all methodology to smooth out the rough patches. My point specifically was to demonstrated for my friend was that while you cannot time the market perfectly, you can certainly make entries and exits that expose your portfolio to the gains and protect your capital from the great swooshes down.

Why have your money with a passive money manager who collects a fee and only puts you in in passive investments? Where's the value if in a down market you are going to lose right along with indexes? Personally, I don't see any value to that and in fact, it seems to me to be pretty darned expensive.

No comments:

Post a Comment